Figure 1: The price P of a product is determined by a balance between production at each price (supply S) and the desires of those with purchasing power at each price (demand D). The diagram shows a positive shift in demand from D1 to D2, resulting in an increase in price (P) and quantity sold (Q) of the product.

Supply and demand stacked in a conceptual chain.

In microeconomics, supply and demand is an economic model of price determination in a market. It postulates that, holding all else equal, in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted. The concept of supply and demand forms the theoretical basis of modern economics.

In macroeconomics, as well, the aggregate demand-aggregate supply model has been used to depict how the quantity of total output and the aggregate price level may be determined in equilibrium.

Graphical representations[edit]

Supply schedule[edit]

A supply schedule, depicted graphically as a supply curve, is a table that shows the relationship between the price of a good and the quantity supplied by producers. Under the assumption of perfect competition, supply is determined by marginal cost: firms will produce additional output as long as the cost of producing an extra unit is less than the market price they receive.

A rise in the cost of raw materials would decrease supply, shifting the supply curve to the left because at each possible price a smaller quantity would be supplied. One may also think of this as a shift up in the supply curve, because the price must rise for producers to supply a given quantity. A fall in production costs would increase supply, shifting the supply curve to the right and down.

Mathematically, a supply curve is represented by a supply function, giving the quantity supplied as a function of its price and as many other variables as desired to better explain quantity supplied. The two most common specifications are:

1) linear supply function, e.g., the slanted line

, and

, and

2) the constant-elasticity[1] supply function (also called isoelastic or log-log or loglinear supply function), e.g., the smooth curve

which can be rewritten as

By its very nature, the concept of a supply curve assumes that firms are perfect competitors, having no influence over the market price. This is because each point on the supply curve answers the question, «If this firm is faced with this potential price, how much output will it sell?» If a firm has market power—in violation of the perfect competitor model—its decision on how much output to bring to market influences the market price. Thus the firm is not «faced with» any given price, and a more complicated model, e.g., a monopoly or oligopoly or differentiated-product model, should be used.

Economists distinguish between the supply curve of an individual firm and the market supply curve. The market supply curve shows the total quantity supplied by all firms, so it is the sum of the quantities supplied by all suppliers at each potential price (that is, the individual firms’ supply curves are added horizontally).

Economists distinguish between short-run and long-run supply curve. Short run refers to a time period during which one or more inputs are fixed (typically physical capital), and the number of firms in the industry is also fixed (if it is a market supply curve). Long run refers to a time period during which new firms enter or existing firms exit and all inputs can be adjusted fully to any price change. Long-run supply curves are flatter than short-run counterparts (with quantity more sensitive to price, more elastic supply).

Common determinants of supply are:

- Prices of inputs, including wages

- The technology used, productivity

- Firms’ expectations about future prices

- Number of suppliers (for a market supply curve)

Demand schedule[edit]

A demand schedule, depicted graphically as a demand curve, represents the amount of a certain good that buyers are willing and able to purchase at various prices, assuming all other determinants of demand are held constant, such as income, tastes and preferences, and the prices of substitute and complementary goods. Generally, consumers will buy an additional unit as long as the marginal value of the extra unit is more than the market price they pay. According to the law of demand, the demand curve is always downward-sloping, meaning that as the price decreases, consumers will buy more of the good.

Mathematically, a demand curve is represented by a demand function, giving the quantity demanded as a function of its price and as many other variables as desired to better explain quantity demanded. The two most common specifications are linear demand, e.g., the slanted line

and the constant-elasticity demand function (also called isoelastic or log-log or loglinear demand function), e.g., the smooth curve

which can be rewritten as

Note that really a demand curve should be drawn with price on the horizontal x-axis, since it is the independent variable. Instead, price is put on the vertical, f(x) y-axis as a matter of unfortunate historical convention.

Just as the supply curve parallels the marginal cost curve, the demand curve parallels marginal utility, measured in dollars.[2] Consumers will be willing to buy a given quantity of a good, at a given price, if the marginal utility of additional consumption is equal to the opportunity cost determined by the price, that is, the marginal utility of alternative consumption choices. The demand schedule is defined as the willingness and ability of a consumer to purchase a given product at a certain time.

The demand curve is generally downward-sloping, but for some goods it is upward-sloping. Two such types of goods have been given definitions and names that are in common use: Veblen goods, goods which because of fashion or signalling are more attractive at higher prices, and Giffen goods, which, by virtue of being inferior goods that absorb a large part of a consumer’s income (e.g., staples such as the classic example of potatoes in Ireland), may see an increase in quantity demanded when the price rises. The reason the law of demand is violated for Giffen goods is that the rise in the price of the good has a strong income effect, sharply reducing the purchasing power of the consumer so that he switches away from luxury goods to the Giffen good, e.g., when the price of potatoes rises, the Irish peasant can no longer afford meat and eats more potatoes to cover for the lost calories.

As with the supply curve, by its very nature the concept of a demand curve requires that the purchaser be a perfect competitor—that is, that the purchaser have no influence over the market price. This is true because each point on the demand curve answers the question, «If buyers are faced with this potential price, how much of the product will they purchase?» But, if a buyer has market power (that is, the amount he buys influences the price), he is not «faced with» any given price, and we must use a more complicated model, of monopsony.

As with supply curves, economists distinguish between the demand curve for an individual and the demand curve for a market. The market demand curve is obtained by adding the quantities from the individual demand curves at each price.

Common determinants of demand are:

- Income

- Tastes and preferences

- Prices of related goods and services

- Consumers’ expectations about future prices and incomes

- Number of potential consumers

- Advertising

History of the curves[edit]

Cournot’s Recherches (1838)

Jenkin’s Graphical Representation (1870)

Marshall’s Principles (1890)

Figure 2. Early supply and demand curves

Since supply and demand can be considered as functions of price they have a natural graphical representation. Demand curves were first drawn by Augustin Cournot in his Recherches sur les Principes Mathématiques de la Théorie des Richesses (1838) – see Cournot competition. Supply curves were added by Fleeming Jenkin in The Graphical Representation of the Laws of Supply and Demand… of 1870. Both sorts of curve were popularised by Alfred Marshall who, in his Principles of Economics (1890), chose to represent price – normally the independent variable – by the vertical axis; a practice which remains common.

If supply or demand is a function of other variables besides price, it may be represented by a family of curves (with a change in the other variables constituting a shift between curves) or by a surface in a higher dimensional space.

Microeconomics[edit]

Figure 3: Supply and Demand

Equilibrium[edit]

Generally speaking, an equilibrium is defined to be the price-quantity pair where the quantity demanded is equal to the quantity supplied. It is represented by the intersection of the demand and supply curves. The analysis of various equilibria is a fundamental aspect of microeconomics:

Market equilibrium: A situation in a market when the price is such that the quantity demanded by consumers is correctly balanced by the quantity that firms wish to supply. In this situation, the market clears.[3]

Changes in market equilibrium:

Practical uses of supply and demand analysis often center on the different variables that change equilibrium price and quantity, represented as shifts in the respective curves. Comparative statics of such a shift traces the effects from the initial equilibrium to the new equilibrium.

Demand curve shifts:

When consumers increase the quantity demanded at a given price, it is referred to as an increase in demand. Increased demand can be represented on the graph as the curve being shifted to the right. At each price point, a greater quantity is demanded, as from the initial curve D1 to the new curve D2. In the diagram, this raises the equilibrium price from P1 to the higher P2. This raises the equilibrium quantity from Q1 to the higher Q2. (A movement along the curve is described as a «change in the quantity demanded» to distinguish it from a «change in demand,» that is, a shift of the curve.) The increase in demand has caused an increase in (equilibrium) quantity. The increase in demand could come from changing tastes and fashions, incomes, price changes in complementary and substitute goods, market expectations, and number of buyers. This would cause the entire demand curve to shift changing the equilibrium price and quantity. Note in the diagram that the shift of the demand curve, by causing a new equilibrium price to emerge, resulted in movement along the supply curve from the point (Q1, P1) to the point (Q2, P2).

If the demand decreases, then the opposite happens: a shift of the curve to the left. If the demand starts at D2, and decreases to D1, the equilibrium price will decrease, and the equilibrium quantity will also decrease. The quantity supplied at each price is the same as before the demand shift, reflecting the fact that the supply curve has not shifted; but the equilibrium quantity and price are different as a result of the change (shift) in demand.

Supply curve shifts:

When technological progress occurs, the supply curve shifts. For example, assume that someone invents a better way of growing wheat so that the cost of growing a given quantity of wheat decreases. Otherwise stated, producers will be willing to supply more wheat at every price and this shifts the supply curve S1 outward, to S2—an increase in supply. This increase in supply causes the equilibrium price to decrease from P1 to P2. The equilibrium quantity increases from Q1 to Q2 as consumers move along the demand curve to the new lower price. As a result of a supply curve shift, the price and the quantity move in opposite directions. If the quantity supplied decreases, the opposite happens. If the supply curve starts at S2, and shifts leftward to S1, the equilibrium price will increase and the equilibrium quantity will decrease as consumers move along the demand curve to the new higher price and associated lower quantity demanded. The quantity demanded at each price is the same as before the supply shift, reflecting the fact that the demand curve has not shifted. But due to the change (shift) in supply, the equilibrium quantity and price have changed.

The movement of the supply curve in response to a change in a non-price determinant of supply is caused by a change in the y-intercept, the constant term of the supply equation. The supply curve shifts up and down the y axis as non-price determinants of demand change.

Partial equilibrium[edit]

Partial equilibrium, as the name suggests, takes into consideration only a part of the market to attain equilibrium.

Jain proposes (attributed to George Stigler): «A partial equilibrium is one which is based on only a restricted range of data, a standard example is price of a single product, the prices of all other products being held fixed during the analysis.»[4]

The supply-and-demand model is a partial equilibrium model of economic equilibrium, where the clearance on the market of some specific goods is obtained independently from prices and quantities in other markets. In other words, the prices of all substitutes and complements, as well as income levels of consumers are constant. This makes analysis much simpler than in a general equilibrium model which includes an entire economy.

Here the dynamic process is that prices adjust until supply equals demand. It is a powerfully simple technique that allows one to study equilibrium, efficiency and comparative statics. The stringency of the simplifying assumptions inherent in this approach makes the model considerably more tractable, but may produce results which, while seemingly precise, do not effectively model real world economic

phenomena.

Partial equilibrium analysis examines the effects of policy action in creating equilibrium only in that particular sector or market which is directly affected, ignoring its effect in any other market or industry assuming that they being small will have little impact if any.

Hence this analysis is considered to be useful in constricted markets.

Léon Walras first formalized the idea of a one-period economic equilibrium of the general economic system, but it was French economist Antoine Augustin Cournot and English political economist Alfred Marshall who developed tractable models to analyze an economic system.

Other markets[edit]

The model of supply and demand also applies to various specialty markets.

The model is commonly applied to wages, in the market for labor. The typical roles of supplier and demander are reversed. The suppliers are individuals, who try to sell their labor for the highest price. The demanders of labor are businesses, which try to buy the type of labor they need at the lowest price. The equilibrium price for a certain type of labor is the wage rate.[5] However, economist Steve Fleetwood revisited the empirical reality of supply and demand curves in labor markets and concluded that the evidence is «at best inconclusive and at worst casts doubt on their existence.» For instance, he cites Kaufman and Hotchkiss (2006): «For adult men, nearly all studies find the labour supply curve to be negatively sloped or backward bending.»[6]

In both classical and Keynesian economics, the money market is analyzed as a supply-and-demand system with interest rates being the price. The money supply may be a vertical supply curve, if the central bank of a country chooses to use monetary policy to fix its value regardless of the interest rate; in this case the money supply is totally inelastic. On the other hand,[7] the money supply curve is a horizontal line if the central bank is targeting a fixed interest rate and ignoring the value of the money supply; in this case the money supply curve is perfectly elastic. The demand for money intersects with the money supply to determine the interest rate.[8]

According to some studies,[9] the laws of supply and demand are applicable not only to the business relationships of people, but to the behaviour of social animals and to all living things that interact on the biological markets[10] in scarce resource environments.

The model of supply and demand accurately describes the characteristic of metabolic systems: specifically, it explains how feedback inhibition allows metabolic pathways to respond to the demand for a metabolic intermediates while minimizing effects due to variation in the supply.[11]

Empirical estimation[edit]

Demand and supply relations in a market can be statistically estimated from price, quantity, and other data with sufficient information in the model. This can be done with simultaneous-equation methods of estimation in econometrics. Such methods allow solving for the model-relevant «structural coefficients,» the estimated algebraic counterparts of the theory. The Parameter identification problem is a common issue in «structural estimation.» Typically, data on exogenous variables (that is, variables other than price and quantity, both of which are endogenous variables) are needed to perform such an estimation. An alternative to «structural estimation» is reduced-form estimation, which regresses each of the endogenous variables on the respective exogenous variables.

Macroeconomic uses[edit]

Demand and supply have also been generalized to explain macroeconomic variables in a market economy, including the quantity of total output and the aggregate price level. The aggregate demand-aggregate supply model may be the most direct application of supply and demand to macroeconomics, but other macroeconomic models also use supply and demand. Compared to microeconomic uses of demand and supply, different (and more controversial) theoretical considerations apply to such macroeconomic counterparts as aggregate demand and aggregate supply. Demand and supply are also used in macroeconomic theory to relate money supply and money demand to interest rates, and to relate labor supply and labor demand to wage rates.

History[edit]

The 256th couplet of Tirukkural, which was composed at least 2000 years ago, says that «if people do not consume a product or service, then there will not be anybody to supply that product or service for the sake of price».[12]

According to Hamid S. Hosseini, the power of supply and demand was understood to some extent by several early Muslim scholars, such as fourteenth-century Syrian scholar Ibn Taymiyyah, who wrote: «If desire for goods increases while its availability decreases, its price rises. On the other hand, if availability of the good increases and the desire for it decreases, the price comes down.»[13]

If desire for goods increases while its availability decreases, its price rises. On the other hand, if availability of the good increases and the desire for it decreases, the price comes down.

Shifting focus to the English etymology of the expression, it has been confirmed that the phrase ‘supply and demand’ was not used by English economics writers until after the end of the 17th century.[14]

In John Locke’s 1691 work Some Considerations on the Consequences of the Lowering of Interest and the Raising of the Value of Money,[15] Locke alluded to the idea of supply and demand, however, he failed to accurately label it as such and thus, he fell short in coining the phrase and conveying its true significance.[16] Locke wrote: “The price of any commodity rises or falls by the proportion of the number of buyer and sellers” and “that which regulates the price… [of goods] is nothing else but their quantity in proportion to [the] Vent.”[16] Locke’s terminology drew criticism from John Law. Law argued that,»The Prices of Goods are not according to the quantity in proportion to the Vent, but in proportion to the Demand.»[17] From Law the demand part of the phrase was given its proper title and it began to circulate among «prominent authorities» in the 1730s.[16] In 1755, Francis Hutcheson, in his A System of Moral Philosophy, furthered development toward the phrase by stipulating that, «the prices of goods depend on these two jointly, the Demand… and the Difficulty of acquiring.»[16]

It was not until 1767 that the phrase «supply and demand» was first used by Scottish writer James Denham-Steuart in his Inquiry into the Principles of Political Economy. He originated the use of this phrase by effectively combining «supply» and «demand» together in a number of different occasions such as price determination and competitive analysis. In Steuart’s chapter entitled «Of Demand», he argues that «The nature of Demand is to encourage industry; and when it is regularly made, the effect of it is, that the supply for the most part is found to be in proportion to it, and then the demand is simple». It is presumably from this chapter that the idea spread to other authors and economic thinkers. Adam Smith used the phrase after Steuart in his 1776 book The Wealth of Nations. In The Wealth of Nations, Smith asserted that the supply price was fixed but that its «merit» (value) would decrease as its «scarcity» increased, this idea by Smith was later named the law of demand. In 1803, Thomas Robert Malthus used the phrase «supply and demand» twenty times in the second edition of the Essay on Population.[16]

And David Ricardo in his 1817 work, Principles of Political Economy and Taxation, titled one chapter, «On the Influence of Demand and Supply on Price».[18] In Principles of Political Economy and Taxation, Ricardo more rigorously laid down the idea of the assumptions that were used to build his ideas of supply and demand. In 1838, Antoine Augustin Cournot developed a mathematical model of supply and demand in his Researches into the Mathematical Principles of Wealth, it included diagrams. It is important to note that the use of the phrase was still rare and only a few examples of more than 20 uses in a single work have been identified by the end of the second decade of the 19th century.[16]

During the late 19th century the marginalist school of thought emerged. The main innovators of this approach were Stanley Jevons, Carl Menger, and Léon Walras. The key idea was that the price was set by the subjective value of a good at the margin. This was a substantial change from Adam Smith’s thoughts on determining the supply price.

In his 1870 essay «On the Graphical Representation of Supply and Demand», Fleeming Jenkin in the course of «introduc[ing] the diagrammatic method into the English economic literature» published the first drawing of supply and demand curves in English,[19] including comparative statics from a shift of supply or demand and application to the labor market.[20] The model was further developed and popularized by Alfred Marshall in the 1890 textbook Principles of Economics.[18]

Criticism[edit]

The philosopher Hans Albert has argued that the ceteris paribus conditions of the marginalist theory rendered the theory itself an empty tautology and completely closed to experimental testing. In essence, he argues, the supply and demand curves (theoretical functions which express the quantity of a product which would be offered or requested for a given price) are purely ontological.[citation needed]

Piero Sraffa’s critique focused on the inconsistency (except in implausible circumstances) of partial equilibrium analysis and the rationale for the upward slope of the supply curve in a market for a produced consumption good.[21] The notability of Sraffa’s critique is also demonstrated by Paul Samuelson’s comments and engagements with it over many years, for example:

- What a cleaned-up version of Sraffa (1926) establishes is how nearly empty are all of Marshall’s partial equilibrium boxes. To a logical purist of Wittgenstein and Sraffa class, the Marshallian partial equilibrium box of constant cost is even more empty than the box of increasing cost.[22]

Modern Post-Keynesians criticize the supply and demand model for failing to explain the prevalence of administered prices, in which retail prices are set by firms, primarily based on a mark-up over normal average unit costs, and aren’t responsive to changes in demand up to capacity.[23]

Some economists criticize the conventional supply and demand theory for failing to explain or anticipate asset bubbles that can arise from a positive feedback loop.[24] Conventional supply and demand theory assumes that expectations of consumers do not change as a consequence of price changes. In scenarios such as the United States housing bubble, an initial price change of an asset can increase the expectations of investors, making the asset more lucrative and contributing to further price increases until market sentiment changes, which creates a positive feedback loop and an asset bubble.[25] Asset bubbles cannot be understood in the conventional supply and demand framework because the conventional system assumes a price change will be self-correcting and the system will snap back to equilibrium.

Paul Cockshott’s critique focuses on the unfalsifiability of the neoclassical model.

In the linear examples given above we have four unknowns: the slope and intercept of both the supply curve and the demand curve.

But because we only have two knowns, price and quantity, any set of supply and demand curves that crosses the point  could explain the data. Hence unfalsifiability.

could explain the data. Hence unfalsifiability.

Cockshott also points out that prices are negatively correlated with quantity due to economies of scale, not positively correlated as the theory suggests.

Finally, Cockshott argues that the theory is needlessly complicated when compared to the labour theory of value, and that having to introduce a notion of the curves shifting amounts to adding epicycles.[26]

See also[edit]

- Capacity utilization

- Consumer theory

- Deadweight loss

- Economic surplus

- Effective demand

- Effect of taxes and subsidies on price

- Elasticity

- Excess demand function

- Externality

- Guanzi (text)

- History of economic thought

- Inverse demand function

- Law of supply

- Neoclassical economics

- Price discovery

- Rationing

- Social cost

- Supply chain

- Supply shock

- Yield management

References[edit]

- ^ The elasticity coefficient, or often just elasticity, is an important parameter in metabolic control analysis, used to express the local response of an enzyme or other chemical reaction to changes in its environment.

- ^ «Marginal Utility and Demand». Retrieved 2007-02-09.

- ^ Mankiw, N.G.; Taylor, M.P. (2011). Economics (2nd ed., revised ed.). Andover: Cengage Learning.

- ^ Jain, T.R. (2006–2007). Microeconomics and Basic Mathematics. New Delhi: VK Publications. p. 28. ISBN 978-81-87140-89-4.

- ^ Kibbe, Matthew B. «The Minimum Wage: Washington’s Perennial Myth». Cato Institute. Retrieved 2007-02-09.

- ^ Fleetwood, Steve (August 2014). «Do labour supply and demand curves exist?». Cambridge Journal of Economics. 38 (5): 1087–113. doi:10.1093/cje/beu003.

- ^ Basij J. Moore, Horizontalists and Verticalists: The Macroeconomics of Credit Money, Cambridge University Press, 1988

- ^ Ritter, Lawrence S.; Silber, William L.; Udell, Gregory F. (2000). Principles of Money, Banking, and Financial Markets (10th ed.). Addison-Wesley, Menlo Park C. pp. 431–38, 465–76. ISBN 978-0-321-37557-5.

- ^ Velev, Milen V. Entropy and free-energy based interpretation of the laws of supply and demand. SN Bus Econ 1, 1 (2021). https://doi.org/10.1007/s43546-020-00009-6

- ^ Noë, R., Hammerstein, P. Biological markets: supply and demand determine the effect of partner choice in cooperation, mutualism and mating. Behav Ecol Sociobiol 35, 1–11 (1994). https://doi.org/10.1007/BF00167053

- ^ Hofmeyr, J.-H.S.; Cornish-Bowden, A. (2000). «Regulating the cellular economy of supply and demand». FEBS Lett. 476 (1): 47–51. doi:10.1111/j.1432-1033.1991.tb21071.x. PMID 1879427.

- ^ C Chendroyaperumal (2010). The First Laws in Economics and Indian Economic Thought – Thirukkural

- ^ a b Hosseini, Hamid S. (2003). «Contributions of Medieval Muslim Scholars to the History of Economics and their Impact: A Refutation of the Schumpeterian Great Gap». In Biddle, Jeff E.; Davis, Jon B.; Samuels, Warren J. (eds.). A Companion to the History of Economic Thought. Malden, MA: Blackwell. pp. 28–45 [28 & 38]. doi:10.1002/9780470999059.ch3. ISBN 978-0-631-22573-7. (citing Hamid S. Hosseini, 1995. «Understanding the Market Mechanism Before Adam Smith: Economic Thought in Medieval Islam,» History of Political Economy, Vol. 27, No. 3, 539–61).

- ^ Thweatt, W.O. (1983). «Origins of the terminology, supply and demand». Scottish Journal of Political Economy. 30 (3): 287–294. doi:10.1111/j.1467-9485.1983.tb01020.x.

- ^ John Locke (1691) Some Considerations on the consequences of the Lowering of Interest and the Raising of the Value of Money

- ^ a b c d e f Groenewegen P. (2008) ‘Supply and Demand’. In: Palgrave Macmillan (eds) The New Palgrave Dictionary of Economics. Palgrave Macmillan, London

- ^ Law, J. (1705). Money and Trade Considered with a Proposal for Supplying the Nation with Money. Edinburgh: Anderson.

- ^ a b Humphrey, Thomas M. (1992). «Marshallian Cross Diagrams and their Uses before Alfred Marshall» (PDF). Economic Review (Mar/Apr): 3–23. Retrieved 2019-07-27.

- ^ A.D. Brownlie and M. F. Lloyd Prichard, 1963. «Professor Fleeming Jenkin, 1833–1885 Pioneer in Engineering and Political Economy,» Oxford Economic Papers, NS, 15(3), p. 211.

- ^ Fleeming Jenkin, 1870. «The Graphical Representation of the Laws of Supply and Demand, and their Application to Labour,» in Alexander Grant, ed., (Scroll to chapter) Recess Studies, ch. VI, pp. 151–85. Edinburgh: Edmonston and Douglas

- ^ Avi J. Cohen, «‘The Laws of Returns Under Competitive Conditions’: Progress in Microeconomics Since Sraffa (1926)?», Eastern Economic Journal, V. 9, N. 3 (Jul.-Sep.): 1983)

- ^ Paul A. Samuelson, «Reply» in Critical Essays on Piero Sraffa’s Legacy in Economics (edited by H. D. Kurz) Cambridge University Press, 2000

- ^ Lee, F. S. (1999). Post Keynesian price theory. Cambridge University Press.

- ^ What Every Economics Student Needs to Know and Doesn’t Get in the Usual Principles Text. Routledge. 2014. pp. 55, 66, 244.

- ^ «Positive Feedback». Investopedia. Retrieved November 13, 2018.

- ^ Paul Cockshott: How the World Works: The Story of Human Labor from Prehistory to the Modern Day. Monthly Review Press, 2020, ISBN 978-1-58367-777-3. pp. 65-68

Further reading[edit]

- Foundations of Economic Analysis by Paul A. Samuelson

- Price Theory and Applications by Steven E. Landsburg ISBN 0-538-88206-9

- An Inquiry into the Nature and Causes of the Wealth of Nations, Adam Smith, 1776 [1]

- Supply and Demand book by Hubert D. Henderson at Project Gutenberg.

External links[edit]

![]()

Look up supply or demand in Wiktionary, the free dictionary.

- Nobel Prize Winner Prof. William Vickrey: 15 fatal fallacies of financial fundamentalism – A Disquisition on Demand Side Economics (William Vickrey)

- Marshallian Cross Diagrams and Their Uses before Alfred Marshall: The Origins of Supply and Demand Geometry by Thomas M. Humphrey

- By what is the price of a commodity determined?, a brief statement of Karl Marx’s rival account

- Supply and Demand by Fiona Maclachlan and Basic Supply and Demand by Mark Gillis, Wolfram Demonstrations Project.

Organizations spend a significant amount of money to determine the level of public demand for their products and services. There are consistent studies and researches conducted to verify if the manufactured product will be saleable. Incorrect estimates can lead to dire results and losses. Supply and demand are both proportionately important to drive the economy.

A Fundamental Concept

Supply and demand patterns form the foundation of the modern economy. The price, utility, and people’s preferences affect the supply and demand patterns.

When there’s a huge demand for a good despite a price-rise the manufacturers will increase the supply.

We will explore supply and demand in great detail in this article. If you are looking to understand supply and demand and how it impacts markets and your business, then you are in the right place.

This article will cover:

- Supply and demand definitions

- Law of supply and demand

- How supply and demand affect each other

- How supply and demand affect market prices

- What if supply is more than demand?

- What if demand is more than supply?

- Exceptions to the law of supply and demand

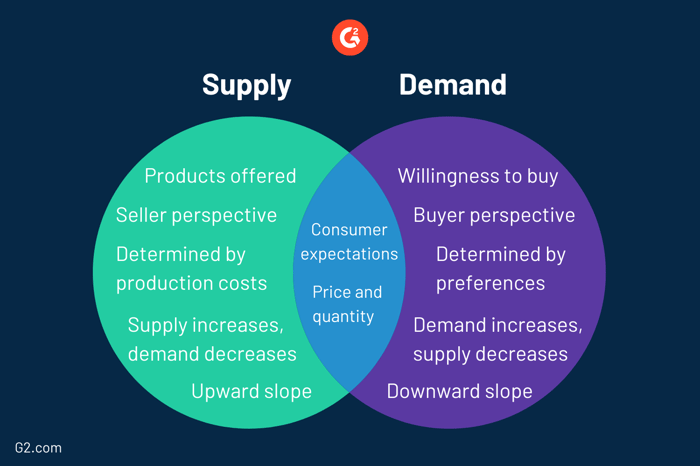

What is Supply?

In economics, supply is a concept that describes the total quantity of goods, or inventory, available to the consumers. Supply depends on the quantity of goods available at a particular price. Because of this fact, supply is closely related to demand. This implies that when the demand for goods increase, the supply also increases. Moreover, supply also increases when the price increases as the manufacturers would like to produce goods that help them maximize their profits.

Factors Affecting Supply

While supply could relate to anything that has competitive market demand, it is usually spoken of in context to goods, labor, or services.

Supply is a concept that is measured through a lot of formulas and is determined through various factors. One such immensely important factor is the price of a product as it plays a crucial role in the process of supply. We often observe that the supply increases with an increase in the price. Apart from the main good, the prices of raw materials and labor also affect the supply. After all, the prices of the related items or services also contribute to the overall price of the main good.

The mathematical formulas for supply establish a relation between supply and the factors affecting it, like the price of the good. Apart from the ones seen in the previous section, the market influences, government rules, and inflation could be other reasons for affecting the supply.

Having learned some basics about supply, let’s move on to its close relative: Demand.

What is Demand?

Just like supply, demand is an economic concept. The readiness and potential of consumers to purchase a specific quantity of a good or service at a specific point in time or over a specific period of time are referred to as demand.

Demand can be categorized as:

Market demand: It signifies the demand for a specific good.

Aggregate demand: Aggregate demand stands for the demand for all the goods.

Factors Affecting Demand

With the increase of supply, the price tends to reduce owing to the continuing demand. Theoretically, the markets will reach a point of balance where the supply is equal to demand for a certain price point. This will mean there is no oversupply and no shortfall either; which in turn ensures a beneficial utility to consumers and maximization of profits for the manufacturers.

Economic concepts- Supply and Demand, are equally responsible for the impact on the prices of goods and services. The association between supply and demand eventually gets balanced. This is called an equilibrium price as per the market economy theory.

One of the primary reasons for consumers to purchase a product is its low price whereas the manufacturers want to maximize their profits by increasing the prices. If the prices increase, the customers may not purchase the particular product and the demand for the product takes a dip. This will lead to a loss for the suppliers as the products are not consumed enough.

Similarly, if the prices go down then the demand may increase but again, the suppliers would be at loss due to reduced profits. Therefore, supply and demand are said to be very closely associated.

Some factors that affect demand are:

- The overall appeal of the good

- Competition faced from rival products

- Financing for the said product

- Quantity available in the market

What is the Law of Supply and Demand?

By definition, Law of supply and demand depicts the association between the sellers and purchasers of a particular good. It is a theory that describes the relationship between the price of a particular good or product and people’s willingness to buy or sell it. In general, people tend to supply more and demand less as prices rise, while the reverse is true if the prices fall.

It is a theory that takes from both: the law of supply and the law of demand.

Law of Supply: On one side, the law of supply states that the higher the cost of the goods, the more is the supply from the sellers.

Law of Demand: On the other side, the law of demand states that the higher the prices, the lower will be the purchases from consumers.

Both these laws aid in determining the prices and quantities of goods traded in the economy.

Law of Supply and Demand: The Difference

Being one of the most fundamental economic laws, the laws of supply and demand are intertwined with almost all economic principles in some way.

The willingness of the consumers to supply and demand a product establishes the market equilibrium. This equilibrium can also be achieved when the suppliers readily supply the amount demanded by the consumers. Yet, numerous factors may affect supply and demand.

|

Law of Supply |

Law of Demand |

|

As the cost of the good increases/decreases, the amount of good produced and sold by producers decreases/increases respectively. |

As the cost of the good increases/decreases, the amount of good purchased by consumers decreases/increases respectively. |

|

Manufacturers or producers prefer to sell at the highest possible cost. |

Consumers prefer to buy at the lowest possible cost. |

|

The price of the good is directly proportional to the supplied amount of the good. |

The price of the good is inversely proportional to the demand of the good. |

What is the Supply and Demand Curve?

The supply and demand curve will require us to consider the supply curve and demand curve independently.

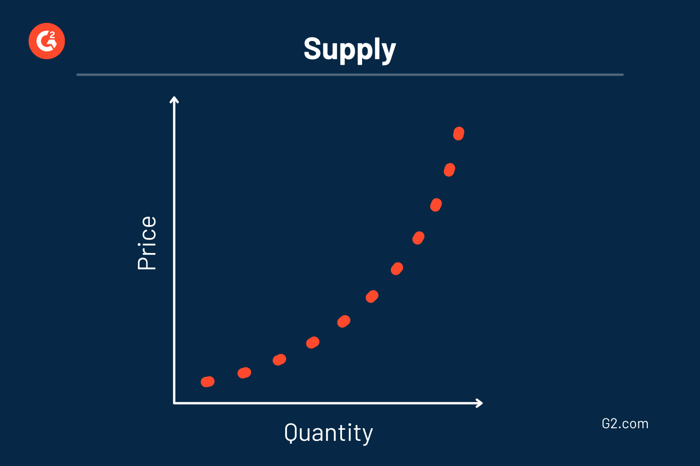

Supply Curve

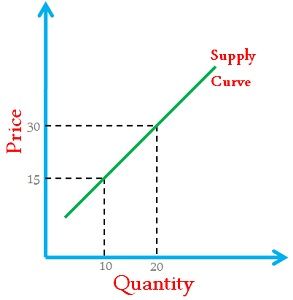

Supply represents the sellers’ perspective of maximizing their profits. A supply curve exhibits the quantity of the goods that a supplier is able and willing to provide for the consumers, at a price rise for a particular time.

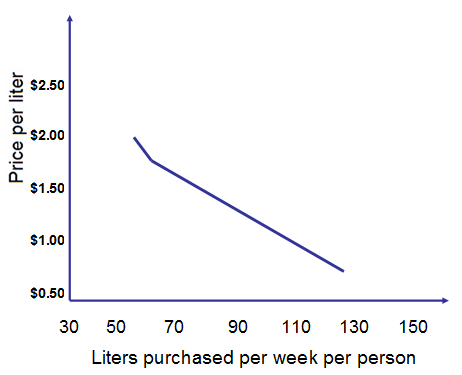

Example:

For simplicity, we assume an economic backdrop where the producer sells directly to consumers. Here’s a schedule that depicts the fuel provided by the suppliers. The suppliers offer 50 liters per customer or consumer each week at the cost of $1.20 per liter. However, if the consumers are willing to pay $2 per liter, then the suppliers will provide 130 liters per week.

|

Cost per liter |

Quantity provided per week in liters |

|

$1.20 |

50 |

|

$1.30 |

60 |

|

$1.50 |

80 |

|

$1.75 |

95 |

|

$2.00 |

130 |

The supply graph for this is shown below:

|

|

The curve is an upward slope indicating a direct relationship between the price and the supply. With the price-rise, the supply rises, and with a fall in price, the supply dives down, too.

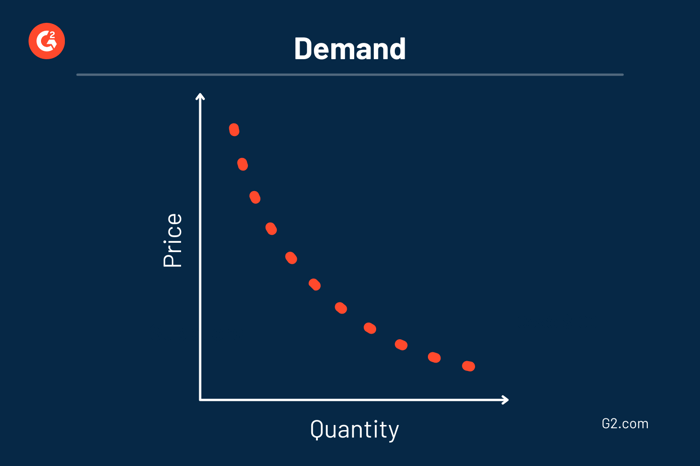

Demand Curve

From the same example, we shall understand the demand curve.

Demand implies the number of products the consumers are willing to buy at varying prices in certain time duration.

If the price of the fuel is $2.00 per liter, people willingly purchase 60 liters per week. In case of a price drop, $1.70 per liter, there may be a rise in consumption of say 70 liters per week. With a further reduction in prices: $1.50, people may purchase up to 75 liters each week.

|

Cost per liter |

Quantity demanded per week in liters |

|

$2.00 |

60 |

|

$1.70 |

70 |

|

$1.50 |

75 |

|

$1.25 |

85 |

|

$1.00 |

100 |

With a reduced price per liter, people tend to make nonessential purchases. In this case, owing to the decline in fuel prices, they may buy surplus fuel or they may undertake unnecessary trips and journeys as the fuel prices fall within the budget bracket. But since the price is the factor that decides the purchasing capacity, if the prices rise again, there will be a dip in the demand.

The graph of this information is as follows:

|

|

The demand curve slopes downward. This indicates an inverse relationship between price and demand.

Equilibrium

Another essential aspect of the demand and supply curve is equilibrium. At this point, the demand and the supply for a good become equal. This means that neither is there a shortage nor a surplus of the good in the market. This equilibrium price can be seen in the following graph:

|

|

What Happens if Supply is More and Demand is Less?

More supply and less demand will lead to a lot of goods left behind for consumption. This scenario results in a surplus availability of the goods.

Surplus may be a result of very high prices of the goods, because of which people do not purchase goods and the demand reduces. In such a case, consumers either start buying substitute products or reduce their average purchase of this good.

Eliminating Surplus: To defeat surplus, the producers or suppliers will have to bring down the prices so that the customers resume their purchases.

What Happens if Demand is More and Supply is Less?

More demand and less supply will lead to lesser goods being available for the consumers resulting in a shortage of goods.

Shortage results when the products are priced very low. However, the chances of the prices shooting up are high as the competition to purchase catalyzes the price rise.

Eliminating Shortage:

The suppliers may restrict the supply so that the prices rise and they register profit, along with balancing out the shortage.

Exceptions to the Rule of Supply and Demand

Having learned about the laws of supply and demand in detail, we come to discuss the exception to the rules in both cases. Let’s start with the exceptions to the law of demand.

Exceptions to Law of Demand

Giffen and Veblen goods are the exceptions in this case. The experts believe that though these are rare occurrences and tough to prove, there are indeed instances where the law of demand gets breached.

Brushing up the concept before we move on: According to the law of demand, the quantity demanded increases when the prices fall; which is indicative of an inverse relationship between the price and quantity.

Giffen Goods

Giffen goods present a scenario where the demand increases even when the prices are increasing. The name comes from Sir Robert Giffen who introduced his observations. He observed that in the early 19th century, the low-wage British workers bought more bread despite the increased prices. This occurrence directly contradicts the Law of Demand.

The reason being that the increased prices of bread left the workers with little amount for meat. So, they compensated for the calories by buying more bread, using up the extra money remaining with them.

Giffen goods are generally regarded as inferior goods, as it reinforces that consumers consume more subpar goods despite the price-rise; this directly contradicts the Law of Demand and is therefore considered an exception.

Veblen Goods

This name also takes from the economist who introduced it. Thorstein Veblen stated that people perceived some higher-priced goods as having greater efficacy. An example of Veblen good is the diamonds. Due to its perceived worth, people will buy diamonds even if the prices keep rising. Veblen goods signify status and opulence and are much more visible in society than the Giffen goods. Luxury cars are another example here.

The Exception to Law of Supply

The Law of Supply states that as the cost of the good increases/decreases, the amount of good supplied decreases/increases respectively. Here are some factors that are exceptions to this law.

Competition: Sellers may reduce the prices of certain goods to stay relevant in the market competition. This disqualifies the law of supply.

Business change: When a business owner is planning to move to another trade, the chances are that he may sell off his stock at a lower price. So, a lot more is available to the new buyer at much lower prices. This cancels the Law of Supply.

Market Control: In other words, a monopoly can lead to a seller controlling the market supply despite the rise in prices. This again nullifies the law.

Perishable goods: Certain goods with an early expiry date may be given away at lower prices. This is done by sellers to avoid being at loss due to the perishability of the goods.

Authoritative Restriction on Quantities: Government regulations or the rules set by the local governing bodies could prohibit the sellers to produce beyond a regulated amount. Also, they may impose restrictions on the prices of some goods so that sellers do not sell the goods above the specified prices.

Artistic Goods: Even if there’s a surge in prices, artistic goods cannot be produced on demand. Therefore, such goods invalidate the law of supply.

Agricultural goods: Being a natural commodity, agricultural products cannot be supplied beyond a limit despite the price increase.

These are some of the areas where the Law of Supply cannot be applied.

Key Takeaways

And that’s a wrap. With this systematic exploration of supply and demand, we pick up the following points from the article:

- Supply is the total quantity of goods or services that are available to the consumers.

- Demand is the consumer’s willingness to buy a product at a given price.

- Both demand and supply work hand-in-hand to determine the prices and the quantities of the goods in the market.

- The Law of Supply states that at higher prices of a good, the producers will supply a larger quantity to the market.

- The Law of Demand is a basic economic principle that states that higher prices will attract lesser demand from the consumers.

- Equilibrium is the stage where the supply and demand become equal.

- The condition when the Supply is more than the Demand is called Surplus.

- The condition where the Demand is more than the Supply is called Shortage.

- Price elasticity of a product is linked to its supply and demand curve.

Hope you have a better understanding of supply and demand, the cornerstones of modern economics and are able to use this understanding to run a better business.

Definition: Supply and demand are economic are the economic forces of the free market that control what suppliers are willing to produce and what consumers are willing and able to purchase.

What Does Supply and Demand Mean?

What is the definition of supply and demand? The term supply refers to how much of a certain product, item, commodity, or service suppliers are willing to make available at a particular price. Demand refers to how much of that product, item, commodity, or service consumers are willing and able to purchase at a particular price.

In other words, supply pertains to how much the producers of a product or service are willing to produce and can provide to the market with limited amount of resources available. Whereas, demand is how much of that product or service the buyers desire to have from the market.

Law of Supply and Demand

Demand and supply play a key role in setting price of a particular product in the market economy. Since demands of buyers are endless, not all that is demanded can be supplied due to scarcity of resources. This is where the relationship of demand and supply plays a significant role, allowing efficient allocation of resources and determining a market price for the product or service, known as equilibrium price. This price reflects the price at which suppliers are willing to supply and the buyers are willing to buy from the market.

The mechanism of determining market price through demand and supply can be better understood by observing the market economic theories.

According to the law of demand, as the price of a product or service rises, the demand of buyers will decrease for it due to limited amount of cash they have to make purchases.

Example 1: A shopkeeper was offering a box of chocolate at price of $20, for which he was able to sell on average 50 boxes every week. He decided to offer 50% discount, decreasing the price to $10. This resulted in increase of his sales to 100 boxes each week.

According to the law of supply, as the price of a product increases, the suppliers will be more willing to supply that product as they can enjoy higher profits by selling that product or service.

Example 2: A factory worker is paid $10 for providing his services to the factory for 50 hours per day. However, due to extra workload, more services were required per day for which the worker would only provide 100 hours if he were paid more i.e. $20.

From this we can conclude that demand has an inverse relationship with price; whereas, supply has a direct relationship with price. Therefore, when both demand and supply are put together, we can determine the equilibrium price, which is the market price of a product or service. This is the point at which the quantity supplied and quantity demanded is exactly equal and the resources are efficiently allocated.

Supply and Demand Graph

Example 3: Jack initiated a hot dog selling business and decided to sell 150 hot dogs per week, pricing each at $30. Other hot dog sellers in the market had been selling hot dogs for $20, which diverted the potential customers away. Jack was left with excess supply of hot dogs with no buyers willing to purchase at price $30.

Example 4: Jennifer offered to pay $10 to the shopkeeper for a CD she wanted to buy. The shopkeeper denied arguing that the costs he incurs to produce one CD are $12 and he will be left with nothing but a loss of $2. So the shopkeeper was only ready to accept minimum of $20 for each CD, which is the market rate.

Summary Definition

Define Supply and Demand: Supply & Demand means the amount of goods or services companies are willing to produce and the amount of goods or services that consumers are willing to purchase.

Contents

- What Does Supply and Demand Mean?

- Law of Supply and Demand

- Supply and Demand Curve Example

- Supply and Demand Graph

- Summary Definition

When thinking of markets, you may wonder: what is the driving force behind the relationship between the production and consumption that makes up markets and ultimately economies? This explanation will introduce you to one of the foundational concepts of economics — supply and demand, which is essential in both basic and advanced economics, as well as in your everyday life. Ready? Then read on!

Supply and Demand Definition

Supply and demand is a simple concept that describes how much of something people want to buy (demand) and how much of that thing is available for sale (supply).

Supply and demand is an economic model that describes the relationship between the quantity of a good or service that producers are willing to offer for sale and the quantity that consumers are willing and able to buy at different prices, holding all other factors constant.

While the supply and demand definition may sound complex at first, it is a simple model that visualizes the behaviors of producers and consumers in a given market. This model is largely based on the three main elements:

- Supply curve: the function that represents the relationship between the price and the quantity of products or services that producers are willing to supply at any given price point.

- Demand curve: the function that represents the relationship between the price and the quantity of products or services that consumers are willing to purchase at any given price point.

- Equilibrium: the point of intersection between the supply and demand curves, representing the price-quantity point where the market stabilizes.

These are the three core elements that you will need to keep in mind as you work on developing a more comprehensive understanding of the supply and demand model. Keep in mind that these elements are not just random numbers; they are representations of human behavior under the effect of various economic factors that ultimately determines prices and available quantities of commodities.

The Law of Supply and Demand

Behind the interaction between consumers and producers is the theory known as the law of supply and demand. This law is defined by the relationship between the price of a product or service and the willingness of market actors to either provide or consume that product or service based off that price.

You may think of the law of supply and demand as a theory compounded by two complimentary laws, the law of demand and the law of supply. The law of demand states that the higher the price of a good, the lower the quantity consumers will wish to buy. The law of supply, on the other hand, states that the higher the price, the more of that good producers will want to supply. Together, these laws act to drive the price and quantity of goods in the market. The compromise between consumers and producers in price and quantity is known as the equilibrium.

The law of demand states that the higher the price of a good the lower the quantity consumers will wish to buy.

The law of supply states that the higher the price of a good the more producers will want to supply.

Some supply and demand examples include markets for physical goods, where producers supply the product and consumers then purchase it. Another example is markets for various services, where service providers are the producers and users of that service are the consumers.

Regardless of what the commodity that is being transacted, the supply and demand relationship between producers and consumers is what fine-tunes the price and quantity of that commodity available, thus allowing the market for it to exist.

Supply and Demand Graph

The supply and demand graph has two axes: the vertical axis represents the price of the good or service, while the horizontal axis represents the quantity of the good or service. The supply curve is a line that slopes upwards from left to right, indicating that as the price of the good or service increases, producers are willing to supply more of it. The demand curve is a line that slopes downwards from left to right, indicating that as the price of the good or service increases, consumers are willing to demand less of it.

The graph is easily recognizable by its «criss-cross» system of two functions, one representing supply and the other representing demand.

Fig. 1 — Basic Supply and Demand Graph

Fig. 1 — Basic Supply and Demand Graph

Supply and demand schedule

Since the supply and demand functions represent data in a market, you need data points to put on a graph to ultimately draw the functions. To make this process organized and easy to follow, you may want to enter your data points, which are different quantities of product or service demanded and supplied at a range of price points, into a table that you will refer to as a schedule. Take a look at Table 1 below for an example:

| Table 1. Example of a supply and demand schedule | ||

|---|---|---|

| Price ($) | Quantity Supplied | Quantity Demanded |

| 2.00 | 3 | 12 |

| 4.00 | 6 | 9 |

| 6.00 | 9 | 6 |

| 10.00 | 12 | 3 |

Whether you are drawing your supply and demand graph by hand, using a graphing calculator, or even spreadsheets, having a schedule will not only help you stay organized with your data but insure that your graphs are as accurate as they can be.

Demand schedule is a table that shows different quantities of a good or product sought out by consumers at a range of given prices.

Supply schedule is a table that shows different quantities of a good or product that producers are willing to supply at a range of given prices.

Supply and demand curves

Now that you are familiar with supply and demand schedules, the next step is to put your data points into a graph, thus producing a supply and demand graph. You can do this either by hand on paper or let software do the task. Regardless of the method, the outcome will likely look similar to the graph you can see in Figure 2 provided below as an example:

Fig. 2 — Supply and demand graph

As you can see from Figure 2, demand is a downward-sloping function and supply slopes upward. Demand slopes downward mainly due to diminishing marginal utility, as well as the substitution effect, which is characterized by consumers seeking alternatives at cheaper prices as the price of the original product rises.

The Law of Diminishing Marginal Utility states that as consumption of a good or service increases, the utility derived from every additional unit will decrease.

Notice that while both the supply and demand functions in the graph above are linear for the sake of simplicity, you will often see that supply and demand functions can follow different slopes and can often look more like curves rather than simple straight lines, as shown in Figure 3 below. How the supply and demand functions look on a graph depends on what kind of equations provide the best fit for the data sets behind the functions.

Fig. 2 — Non-linear supply and demand functions

Fig. 2 — Non-linear supply and demand functions

Supply and Demand: Equilibrium

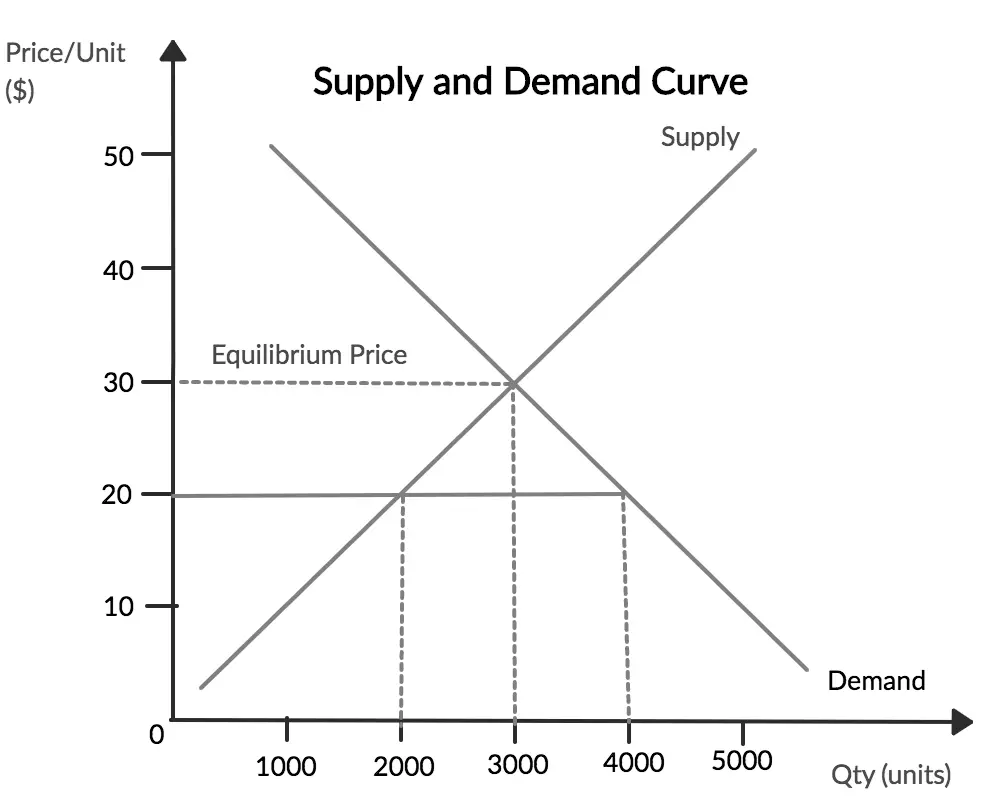

So why graph supply and demand in the first place? Besides visualizing data about consumers’ and producers’ behavior in a market, one important task that a supply and demand graph will help you with is finding and identifying the equilibrium quantity and price in the market.

Equilibrium is the quantity-price point where quantity demanded equals quantity supplied, and thus produce a stabilized balance between the price and quantity of a product or service in the market.

Looking back at the supply and demand graph provided above, you will notice that the point of intersection between the supply and demand functions is labeled as «equilibrium». The equilibrium equating to the point of intersection between the two functions ties into the fact that equilibrium is where consumers and producers (represented by the demand and supply functions, respectively) meet at a compromising price-quantity.

Refer to the mathematical representation of the equilibrium below, where Qs equals quantity supplied, and Qd equals quantity demanded.

Equilibrium occurs when:

(hbox{Qs}=hbox{Qd})

(hbox{Quantity Supplied}=hbox{Quantity Deamnded})

There are many other valuable conclusions that you can gather from a supply and demand graph, such as surpluses and shortages.

To learn more about surpluses as well as get a deeper understanding of equilibrium, take a look at our explanation on Market Equilibrium and Consumer and Producer Surplus.

Determinants of demand and supply

Changes in the price of a good or a service will lead to a movement along the supply and demand curves. However, changes in the demand and supply determinants will shift either the demand or the supply curves respectively.

Shifters of supply and demand

Determinants of demand include but are not limited to:

- Changes in prices of related goods

- Consumers’ income

- Consumers’ tastes

- Consumers’ expectations

- Number of consumers in the market

To learn more about how changes in demand determinants affect the demand curve check out our explanation — Shifts in Demand

Determinants of supply include but are not limited to:

- Changes in input prices

- Price of related goods

- Changes in technology

- Producers’ expectations

- Number of producers in the market

To learn more about how changes in supply determinants affect the supply curve check out our explanation — Shifts in Supply

The elasticity of supply and demand

As you become more familiar with supply and demand and interpreting their corresponding graphs, you will notice that different supply and demand functions vary in the steepness of their slopes and curvatures. The steepness of these curves reflects the elasticity of each supply and demand.

Elasticity of supply and demand is a measure that represents how responsive or sensitive each of the functions is to changes in various economic factors, such as price, income, expectations, and others.

While both supply and demand are subject to variation in elasticity, it is interpreted differently for each function.

Elasticity of demand

Elasticity of demand represents how sensitive demand is to a change in various economic factors in the market. The more the consumers are responsive to an economic change, in terms of how much that change affects the consumers’ willingness to still purchase that good, the more elastic the demand. Alternatively, the less flexible the consumers are to economic fluctuations for a specific good, meaning they likely have to continue purchasing that good regardless of the changes, the more inelastic demand is.

You can calculate the price elasticity of demand, for example, simply by dividing the percentage change in quantity demanded by the percentage change in price, as shown by the formula below:

The triangle symbol delta means change. This formula refers to the percentage change, such as a 10% decrease in price.

(hbox{Price elasticity of demand}=frac{hbox{% $Delta$ Quantity demanded}}{hbox{% $Delta$ Price}})

There are three main types of elasticity of demand that you will need to focus on for now:

- Price elasticity: measures how much the quantity demanded of a good varies due to changes in the good’s price. Learn more in our explanation on Price elasticity of demand.

- Income elasticity: measures how much the quantity demanded of a specific good varies due to changes in income of the consumers of that good. Check out our explanation on Income Elasticity of Demand.

- Cross elasticity: measures how much the quantity demanded of one good changes in response to a change in the price of another good. See more in our explanation for Cross Elasticity of Demand.

Elasticity of demand measures how sensitive demand is to changes in various economic factors in the market.

Elasticity of supply

Supply can also vary in elasticity. One specific type of elasticity of supply is price elasticity of supply, which measures how responsive producers of a certain commodity are to a change in market price for that commodity.

You can calculate price elasticity of supply by dividing the percentage change in quantity supplied by the percentage change in price, as shown by the formula below:

The triangle symbol delta means change. This formula refers to the percentage change, such as a 10% decrease in price.

(hbox{Price elasticity of Supply}=frac{hbox{% $Delta$ Quantity Supplied}}{hbox{% $Delta$ Price}})

There are numerous factors that can affect price elasticity of supply, such as availability of resources needed for production, changes in demand for the product that the firm produces, and innovations in technology.

To learn more about these factors as well as how to interpret your results from calculating elasticity of supply, see our explanation on Price Elasticity of Supply.

Elasticity of supply measures how sensitive supply is to changes in various economic factors in the market.

Supply and Demand Examples

Let’s consider and example of the supply and demand of ice-cream in a small city in the UK.

| Table 2. Supply and Demand Example | ||

|---|---|---|

| Price ($) | Quantity Demanded (per week) | Quantity Supplied (per week) |

| 2 | 2000 | 1000 |

| 3 | 1800 | 1400 |

| 4 | 1600 | 1600 |

| 5 | 1400 | 1800 |

| 6 | 1200 | 2000 |

At a price of $2 per scoop, there is excess demand for ice cream, meaning that consumers want to buy more ice cream than suppliers are willing to provide. This shortage will cause the price to increase.

As the price increases, the quantity demanded decreases and the quantity supplied increases, until the market reaches an equilibrium price of $4 per scoop. At this price, the quantity of ice cream that consumers want to buy is exactly equal to the quantity that suppliers are willing to provide, and there is no excess demand or supply.

If the price were to increase further to $6 per scoop, there would be excess supply, meaning that suppliers are willing to provide more ice cream than consumers want to buy, and this surplus will cause the price to decrease until it reaches a new equilibrium.

The concept of supply and demand is relevant throughout the entire field of economics, and that includes macroeconomics and economic government policies.

Supply and Demand Example: Global Oil Prices

From 1999 to 2007, the price of oil increased due to rising demand from countries like China and India, and by 2008, it reached an all-time high of $147 a barrel. However, the financial crisis of 2007-2008 led to a decline in demand, causing the price of oil to plummet to $34 a barrel by December 2008. After the crisis, the price of oil rebounded and rose to $82 a barrel in 2009. Between 2011 and 2014, the price of oil remained mostly between $90 and $120 due to demand from emerging economies, especially China. However, by 2014, oil production from unconventional sources like hydraulic fracturing in the United States caused a significant increase in supply, leading to a decline in demand and a subsequent drop in oil prices. In response, OPEC members increased their oil production to try and maintain their market share, causing a surplus of oil and further driving down prices. This demonstrates the relationship between supply and demand, where an increase in demand results in an increase in prices, and an increase in supply leads to a decrease in prices.

Effect of Government Policies on Supply and Demand

Governments may intervene in the course of economies in order to correct for undesirable effects of the current economic climates, as well as attempt to optimize future outcomes. There are three main tools that regulatory authorities may use to create targeted changes in the economy:

- Regulations and policies

- Taxes

- Subsidies

Each of these tools may cause either positive or negative changes in the cost of production of various goods. These changes will impact the behavior of producers, which will ultimately affect the price in the market. You can learn more about the effects of these factors on supply in our explanation of Shift in Supply.

The change in market price, in turn, will likely have an effect on consumers’ behavior and subsequently, demand. See more on what factors affect demand and how, as well the extent to which these factors will influence demand based on various circumstances, in our explanations on Shifts in Demand and Price Elasticity of Demand.

Thus, government policies can have a domino-like effect on supply and demand that can entirely change the state of markets. To find out more about this, check out our explanation on The Effects of Government Intervention in Markets.

Government policies may also affect property rights to various resources. Examples of property rights include copyright and patents, which can be applied to intellectual property as well as physical objects. Owning patents or copyrights grants enables exclusivity over the production of a good or service, which leaves consumers with fewer options in the market. This will likely result in the market price increasing, as consumers will have no other choice but to take the price and make a purchase.

Supply and Demand — Key takeaways

- Supply and demand is the relationship between the quantities of products or services that producers are willing to provide versus the quantities that consumers are willing to obtain at a range of various prices.

- The supply and demand model consists of three basic elements: the supply curve, the demand curve, and the equilibrium.

- The equilibrium is the point where supply meets demand and is thus the price-quantity point where the market stabilizes.

- The law of demand states that the higher the price of a good the lower the quantity consumers will wish to buy.

- The law of supply states that the higher the price of a good the more producers will want to supply.

![]()

![]()

- Entertainment & Pop Culture

- Geography & Travel

- Health & Medicine

- Lifestyles & Social Issues

- Literature

- Philosophy & Religion

- Politics, Law & Government

- Science

- Sports & Recreation

- Technology

- Visual Arts

- World History

- On This Day in History

- Quizzes

- Podcasts

- Dictionary

- Biographies

- Summaries

- Top Questions

- Infographics

- Demystified

- Lists

- #WTFact

- Companions

- Image Galleries

- Spotlight

- The Forum

- One Good Fact

- Entertainment & Pop Culture

- Geography & Travel

- Health & Medicine

- Lifestyles & Social Issues

- Literature

- Philosophy & Religion

- Politics, Law & Government

- Science

- Sports & Recreation

- Technology

- Visual Arts

- World History

- Britannica Explains

In these videos, Britannica explains a variety of topics and answers frequently asked questions. - Britannica Classics

Check out these retro videos from Encyclopedia Britannica’s archives. - Demystified Videos

In Demystified, Britannica has all the answers to your burning questions. - #WTFact Videos

In #WTFact Britannica shares some of the most bizarre facts we can find. - This Time in History

In these videos, find out what happened this month (or any month!) in history.

- Student Portal

Britannica is the ultimate student resource for key school subjects like history, government, literature, and more. - COVID-19 Portal

While this global health crisis continues to evolve, it can be useful to look to past pandemics to better understand how to respond today. - 100 Women

Britannica celebrates the centennial of the Nineteenth Amendment, highlighting suffragists and history-making politicians. - Saving Earth

Britannica Presents Earth’s To-Do List for the 21st Century. Learn about the major environmental problems facing our planet and what can be done about them! - SpaceNext50

Britannica presents SpaceNext50, From the race to the Moon to space stewardship, we explore a wide range of subjects that feed our curiosity about space!

Supply and demand form the most fundamental concepts of economics. Whether you are an academic, farmer, pharmaceutical manufacturer, or simply a consumer, the basic premise of supply and demand equilibrium is integrated into your daily actions. Only after understanding the basics of these models can the more complicated aspects of economics be mastered.

Explaining Demand

Although most explanations typically focus on explaining the concept of supply first, understanding demand is more intuitive for many, and thus helps with subsequent descriptions.

The figure above depicts the most basic relationship between the price of a good and its demand from the standpoint of the consumer. This is actually one of the most important differences between the supply curve and the demand curve. Whereas supply graphs are drawn from the perspective of the producer, demand is portrayed from the perspective of the consumer.

As the price of a good increases, the demand for the product will—except for a few obscure situations—decrease. For purposes of our discussion, let’s assume the product in question is a television set. If TVs are sold for the cheap price of $5 each, then a large number of consumers will purchase them at a high frequency. Most people would even buy more TVs than they need, putting one in every room and perhaps even some in storage.

Essentially, because everyone can easily afford a TV, the demand for these products will remain high. On the other hand, if the price of a television set is $50,000, this gadget will be a rare consumer product as only the wealthy will be able to afford the purchase. While most people would still like to buy TVs, at that price, demand for them would be extremely low.

Of course, the above examples take place in a vacuum. A pure example of a demand model assumes several conditions. First, product differentiation does not exist—there is only one type of product sold at a single price to every consumer. Second, in this closed scenario, the item in question is a basic want and not an essential human necessity such as food (although having a TV provides a definite level of utility, it is not an absolute requirement). Third, the good does not have a substitute and consumers expect prices to remain stable into the future.

Explaining Supply

The supply curve functions in a similar fashion, but it considers the relationship between the price and available supply of an item from the perspective of the producer rather than the consumer.

When prices of a product increase, producers are willing to manufacture more of the product to realize greater profits. Likewise, falling prices depress production as producers may not be able to cover their input costs upon selling the final good. Going back to the example of the television set, if the input costs to produce a TV are set at $50 plus the variable costs of labor, production would be highly unprofitable when the selling price of the TV drops below the $50 mark.

On the other hand, when prices are higher, producers are encouraged to increase their levels of activity to reap more benefit. For example, if television prices are $1,000, manufacturers can focus on producing television sets in addition to other possible ventures. Keeping all variables the same but increasing the selling price of the TV to $50,000 would benefit the producers and provide the incentive to build more TVs. The behavior to seek maximum amounts of profits forces the supply curve to be upward sloping.

An underlying assumption of the theory lies in the producer taking on the role of a price taker. Rather than dictating prices of the product, this input is determined by the market and suppliers only face the decision of how much to actually produce, given the market price. Similar to the demand curve, optimal scenarios are not always the case, such as in monopolistic markets.

Finding an Equilibrium

Consumers typically look for the lowest cost, while producers are encouraged to increase outputs only at higher costs. Naturally, the ideal price a consumer would pay for a good would be «zero dollars.» However, such a phenomenon is unfeasible as producers would not be able to stay in business. Producers, logically, seek to sell their products for as much as possible. However, when prices become unreasonable, consumers will change their preferences and move away from the product. A proper balance must be achieved whereby both parties are able to engage in ongoing business transactions to the benefit of consumers and producers. (Theoretically, the optimal price that results in producers and consumers achieving the maximum level of combined utility occurs at the price where the supply and demand lines intersect. Deviations from this point result in an overall loss to the economy commonly referred to as a deadweight loss.

Law or Theory?

The law of supply and demand is actually an economic theory that was popularized by Adam Smith in 1776. The principles of supply and demand have been shown to be very effective in predicting market behavior. However, there are multiple other factors that affect markets on both a microeconomic and a macroeconomic level. Supply and demand heavily guide market behavior, but do not outright determine it.

Another way of looking at the laws of supply and demand is by considering them a guide. While they are only two factors influencing market conditions, they are very important factors. Smith referred to them as the invisible hand that guides a free market. However, if the economic environment is not a free market, supply and demand are not nearly as influential. In socialist economic systems, the government typically sets prices for commodities, regardless of the supply or demand conditions.

This creates problems because the government is not always able to control supply or demand. This is evident when examining Venezuela’s food shortages and high inflation rates from 2010. The country attempted to take over the food supply from private vendors and establish price controls but suffered crippling shortages and accusations of corruption as a result. Supply and demand still very much affected the situation in Venezuela but were not the only influences.

The principles of supply and demand have been illustrated repeatedly over centuries of different market conditions. However, the current economy is more global than it has ever been, and macroeconomic forces can be difficult to predict. Supply and demand are effective indicators, but not concrete predictors.

The Bottom Line

The theory of supply and demand relates not only to physical products such as television sets and jackets but also to wages and the movement of labor. More advanced theories of micro and macroeconomics often adjust the assumptions and appearance of the supply and demand curve to properly illustrate concepts like economic surplus, monetary policy, externalities, aggregate supply, fiscal stimulation, elasticity, and shortfalls. Before studying those more complex issues, the basics of supply and demand must be properly understood.

If a product is being sold but there’s no one around to buy it, does it really exist?