Excel for Microsoft 365 Excel for Microsoft 365 for Mac Excel for the web Excel 2021 Excel 2021 for Mac Excel 2019 Excel 2019 for Mac Excel 2016 Excel 2016 for Mac Excel 2013 Excel 2010 Excel 2007 Excel for Mac 2011 Excel Starter 2010 More…Less

This article describes the formula syntax and usage of the PPMT function in Microsoft Excel.

Description

Returns the payment on the principal for a given period for an investment based on periodic, constant payments and a constant interest rate.

Syntax

PPMT(rate, per, nper, pv, [fv], [type])

Note: For a more complete description of the arguments in PPMT, see PV.

The PPMT function syntax has the following arguments:

-

Rate Required. The interest rate per period.

-

Per Required. Specifies the period and must be in the range 1 to nper.

-

Nper Required. The total number of payment periods in an annuity.

-

Pv Required. The present value — the total amount that a series of future payments is worth now.

-

Fv Optional. The future value, or a cash balance you want to attain after the last payment is made. If fv is omitted, it is assumed to be 0 (zero), that is, the future value of a loan is 0.

-

Type Optional. The number 0 or 1 and indicates when payments are due.

|

Set type equal to |

If payments are due |

|---|---|

|

0 or omitted |

At the end of the period |

|

1 |

At the beginning of the period |

Remarks

Make sure that you are consistent about the units you use for specifying rate and nper. If you make monthly payments on a four-year loan at 12 percent annual interest, use 12%/12 for rate and 4*12 for nper. If you make annual payments on the same loan, use 12% for rate and 4 for nper.

Examples

Copy the example data in the following table, and paste it in cell A1 of a new Excel worksheet. For formulas to show results, select them, press F2, and then press Enter. If you need to, you can adjust the column widths to see all the data.

|

Data |

Argument description |

|

|---|---|---|

|

10% |

Annual interest rate |

|

|

2 |

Number of years for the loan |

|

|

$2,000.00 |

Amount of loan |

|

|

Formula |

Description |

Result |

|

=PPMT(A2/12, 1, A3*12, A4) |

Principal payment for month 1 of the loan |

($75.62) |

|

Data |

Argument description |

|

|

8% |

Annual interest rate |

|

|

10 |

Number of years for the loan |

|

|

$200,000.00 |

Amount of loan |

|

|

Formula |

Description (Result) |

Live Result |

|

=PPMT(A8, A9, 10, A10) |

Principal payment for year 10 of the loan |

($27,598.05) |

Need more help?

Summary

The Excel PPMT function can be used to calculate the principal portion of a given loan payment. For example, you can use PPMT to get the principal amount of a payment for the first period, the last period, or any period in between.

Purpose

Get principal payment in given period

Return value

Arguments

- rate — The interest rate per period.

- per — The payment period of interest.

- nper — The total number of payments for the loan.

- pv — The present value, or total value of all payments now.

- fv — [optional] The cash balance desired after last payment is made. Defaults to 0.

- type — [optional] When payments are due. 0 = end of period. 1 = beginning of period. Default is 0.

Syntax

=PPMT(rate, per, nper, pv, [fv], [type])

Usage notes

The Excel PPMT function is used to calculate the principal portion of a given loan payment. For example, you can use PPMT to get the principal amount of a payment for the first period, the last period, or any period in between. The period of interest is provided with the per argument, which must be a number between 1 and the total number of payments (nper).

Notes

- Be consistent with inputs for rate. For example, for 5-year loan with 4.5% annual interest, enter the rate as 4.5%/12.

- By convention, the loan value (pv) is entered as a negative value.

Author![]()

Dave Bruns

Hi — I’m Dave Bruns, and I run Exceljet with my wife, Lisa. Our goal is to help you work faster in Excel. We create short videos, and clear examples of formulas, functions, pivot tables, conditional formatting, and charts.

I just wanted to say thanks for simplifying the learning process for me! Your website is a life saver!

Get Training

Quick, clean, and to the point training

Learn Excel with high quality video training. Our videos are quick, clean, and to the point, so you can learn Excel in less time, and easily review key topics when needed. Each video comes with its own practice worksheet.

View Paid Training & Bundles

Help us improve Exceljet

The PPMT function in Excel is a financial function used to calculate a principal’s payment. The value returned by this function is an integer value. For instance, you can utilize the PPMT function to get the principal amount of an installment for the first period, the last period, or any period between.

For example, suppose the loan amount is $50,000 in cell B1, and the interest rate is 5% in cell B2. The period of the loan taken in cell B3 is 10 years. Then, we can calculate the principal amount for 1 month of the loan using the PPMT Excel function as follows:

=PPMT(B2/12,1,B3*12,B1)

= $321.99.

Table of contents

- PPMT Function Excel

- Syntax

- Explanation

- How to Use the PPMT Function in Excel? (with Examples)

- Example #1

- Example# 2

- Things to Remember

- Recommended Articles

Syntax

Explanation

The PPMT function in Excel has the same fields as the PPMT in Excel except for an extra field – ‘Per.’

| Arguments | Description |

|---|---|

| Rate | Interest Rate of the Loan |

| Per | Specific payment period |

| Nper | It is the total number of payment that has to be made |

| PV (Present Value) | Amount of the loan (principal amount) |

| FV (Future Value) | Amount as a future value that wants to have left after final payment |

| Type | Whether the payments are made at the beginning (1) or end of the month (0) |

“Per” is the specific pay period for which one wants to compute the amount paid towards the principal. FV in ExcelThe FV function in Excel is a built-in financial function that can also be referred to as the future value function. This function is very useful in calculating the future value of any investment made by anyone. It has some dependent arguments, which are the constant interest, periods, and payments.read more is an optional argument. If omitted, the fv takes on the default value 0.

How to Use the PPMT Function in Excel? (with Examples)

You can download this PPMT Excel Template here – PPMT Excel Template

Example #1

Suppose we need to calculate the payments on the principal for months 1 and 2 on a $10,000 loan, which is to be paid off in full after 3 years with the monthly payment of $500. Interest is charged at a rate of 5% per year. The loan repayments are to be made at the end of each month.

To calculate this, we will use the PPMT in Excel.

Applying the PPMT function with all input values as shown above for every month’s installment, the principal amount for each month.

Similarly, applying the PPMT function to other periods, we also have the principal amount of each period, as shown below.

As you can see above, for each period, the principal amount which totals the amount as the loan amount, which is $200,000.

Example# 2

If the loan amount is $10,000 with an interest rate of 10% and the loan period is 2 years. Then the principal amount for 1 month of the loan will be calculated using the PPMT in Excel, as shown below.

Using the PPMT function, we compute the principal amount for the 1 month.

Here, the fv is optional. Since there is no future value, we took it as 0, and the type is 0 as the payment is made at the end of the month. Even if we skip the last two arguments still, we will get the desired result.

Things to Remember

- The input rate has to be consistent. If the payments are made quarterly, it will convert the annual interest rate into the quarterly rate (rate%/4), and the period number has to be converted from years to quarters (=per*4).

- By convention, the loan value (pv) is entered as negative.

Recommended Articles

This article is a guide to PPMT Function in Excel. Here, we discuss the PPMT formula Excel, how to use the PPMT function, and practical examples and downloadable Excel templates. You can have a look at other articles on Excel functions: –

- Excel NPER FunctionNPER, commonly known as the number of payment periods for a loan, is a financial term and an inbuilt financial function in Excel that can be used to calculate NPER for any loan. This formula takes rate, payment made, present value and future value as input from a user.read more

- Excel PMT FormulaPMT function is an advanced financial function to calculate the monthly payment against the simple loan amount. You have to provide basic information, including loan amount, interest rate, and duration of payment, and the function will calculate the payment as a result.read more

- Mortgage Calculator ExcelIn Excel, a mortgage calculator is not a built-in feature. The amortization schedule is required in order to create the categories column, into which all of the categories and data can be entered. Then, in one cell, we can use the mortgage calculation formula.read more

- Excel Mathematical FunctionMathematical functions in excel refer to the different expressions used to apply various forms of calculation. The seven frequently used mathematical functions in MS excel are SUM, AVERAGE, AVERAGEIF, COUNTA, COUNTIF, MOD, and ROUND.read more

- XML in ExcelExcel has made it very easy for us to import the data in XML to excel in the form of tables or databases. XML is basically an external data and it can be imported to excel from the data tab under the «get external data tab from data from other sources» section.read more

Reader Interactions

Excel PPMT Function

- Summary.

- Get principal payment in given period.

- The principal payment.

- =PPMT (rate, per, nper, pv, [fv], [type])

- rate – The interest rate per period.

- The Excel PPMT function is used to calculate the principal portion of a given loan payment.

Contents

- 1 What is the formula for PPMT?

- 2 How do I use Ipmt in Excel?

- 3 What is the difference between PMT and PPMT functions in excel?

- 4 What does Nper function do?

- 5 What is the difference between Ipmt and PPMT?

- 6 What does PPMT stand for?

- 7 What does Nper stand for?

- 8 Why do we use freeze panes in Excel?

- 9 How do you calculate PMT manually?

- 10 What is PER in PPMT function?

- 11 How do you use Nper function?

- 12 What does FV mean in Excel?

- 13 How do you calculate semi annual pay in Excel?

- 14 What is PMT PPMT and Ipmt?

- 15 How do I write an IFS statement in Excel?

- 16 What does type stand for in Excel?

- 17 What is type in Excel PMT?

What is the formula for PPMT?

Examples

| Data | Argument description |

|---|---|

| Formula | Description |

| =PPMT(A2/12, 1, A3*12, A4) | Principal payment for month 1 of the loan |

| Data | Argument description |

| 8% | Annual interest rate |

How do I use Ipmt in Excel?

The formula to be used will be =IPMT( 5%/12, 1, 60, 50000). In the example above: As the payments are made monthly, it was necessary to convert the annual interest rate of 5% into a monthly rate (=5%/12), and the number of periods from years to months (=5*12).

What is the difference between PMT and PPMT functions in excel?

Whereas the PMT function tells you how much each payment will be, the PPMT function tells you how much of the principal is being paid in any given pay period. (To find out the inverse of this – how much of the interest is being paid in any given pay period – you can use an IPMT function.)

What does Nper function do?

The Excel NPER function is a financial function that returns the number of periods for a loan or investment. You can use the NPER function to get the number of payment periods for a loan, given the amount, the interest rate, and periodic payment amount.type – [optional] When payments are due.

What is the difference between Ipmt and PPMT?

IPMT calculates the interest amount and PPMT calculates the capital amount so you can always determine the proportions for each payment.

What does PPMT stand for?

PPMT

| Acronym | Definition |

|---|---|

| PPMT | Pre and Post Massage Test (urology) |

| PPMT | Prenylated Protein Carboxyl Methyltransferase |

| PPMT | Pre-and Post-Mobilization Training (US DoD) |

| PPMT | Parallel Path Magnetic Technology (QM Power Inc.) |

What does Nper stand for?

Number of Periods

NPER in excel is one of the Financial functions in excel. NPER stands for “Number of Periods.” The number of periods required to clear the loan amount at the specified interest rate and specified monthly EMI amount.

Why do we use freeze panes in Excel?

To Use Freeze Panes:

Choose from the following options: Freeze Panes: Lock more than one column or row (select the row below the last row you want to freeze and/or to the right of the last column you want to freeze). Freeze Top Row: Only lock the top row. Freeze First Column: Only lock the first column.

How do you calculate PMT manually?

Suppose you are paying a quarterly instalment on a loan of Rs 10 lakh at 10% interest per annum for 20 years. In such a case, instead of 12, you should divide the rate by four and multiply the number of years by four. The equated quarterly instalment for the given figures will be =PMT(10%/4, 20*4, 10,00,000).

What is PER in PPMT function?

The Excel PPMT function can be used to calculate the principal portion of a given loan payment. For example, you can use PPMT to get the principal amount of a payment for the first period, the last period, or any period in between.per – The payment period of interest. nper – The total number of payments for the loan.

How do you use Nper function?

The NPER function uses the following arguments:

- Rate (required argument) – This is the interest rate per period.

- Pmt (required argument) – The payment made each period.

- Pv (required argument) – The present value, or the lump-sum amount that a series of future payments is worth right now.

What does FV mean in Excel?

FV, one of the financial functions, calculates the future value of an investment based on a constant interest rate. You can use FV with either periodic, constant payments, or a single lump sum payment. Use the Excel Formula Coach to find the future value of a series of payments.

How do you calculate semi annual pay in Excel?

- Weekly payment: =PMT(8%/52, 3*52, 5000)

- Monthly payment: =PMT(8%/12, 3*12, 5000)

- Quarterly payment: =PMT(8%/4, 3*4, 5000)

- Semi-annual payment: =PMT(8%/2, 3*2, 5000) In all cases, the balance after the last payment is assumed to be $0, and the payments are due at the end of each period.

What is PMT PPMT and Ipmt?

PMT calculates the fixed monthly repayment of a loan taken out over a certain timescale at a fixed interest rate.IPMT calculates the interest amount and PPMT calculates the capital amount so you can always determine the proportions for each payment.

How do I write an IFS statement in Excel?

How to use the IFS Function in Excel? The formula used is: IFS(A2>80,”A”,A2>70,”B”,A2>60,”C”,A2>50,”D”,A2>40,”E”,A2>30,”F”), which says that if cell A2 is greater than 80 then return an “A” and so on.

What does type stand for in Excel?

The Microsoft Excel TYPE function returns the type of a value. The TYPE function is a built-in function in Excel that is categorized as an Information Function. It can be used as a worksheet function (WS) in Excel.

What is type in Excel PMT?

The Excel PMT function is a financial function that returns the periodic payment for a loan.type – [optional] When payments are due. 0 = end of period. 1 = beginning of period. Default is 0.

What is the Excel PPMT Function?

The PPMT Function in Excel returns the periodic principal payments owed on a loan, assuming fixed interest rate pricing and consistent payments.

How to Use PPMT Function in Excel (Step-by-Step)

The Excel “PPMT” function calculates the principal payments required to be paid on a loan.

The borrower, as part of the financing arrangement, is contractually obligated to pay interest on a traditional loan and portions of the principal until the entire loan principal is repaid.

For instance, a consumer that takes out a mortgage or auto loan to finance a purchase must make monthly payments to the lender until the principal is repaid in full, while servicing interest expense obligations simultaneously.

But while the interest paid in each period is based on the outstanding principal balance, the interest payments themselves do not reduce the principal.

In the PPMT function, there are two notable assumptions regarding the loan.

- Fixed Interest Rate → The loan is assumed to have a fixed interest rate (i.e. the rate remains constant and unaffected by a benchmark rate, as in the case of debt securities priced with floating interest rates).

- Constant Payment Value → The other assumption is that the total payments are constant throughout the term of the borrowing, i.e. akin to installment payments, where the payment dates and amounts due are fixed and predictable.

Sources of Loan Yield: Interest vs. Principal Payments

The yield earned by a lender on a loan issuance stems primarily from two sources:

- Periodic Interest Payments → The interest represents income to the lender (i.e. ”inflow of cash”) and the dollar amount charged is a function of the interest rate, which reflects the riskiness of providing capital in the form of debt to the borrower (i.e. credit rating and default risk). Yet, in spite of the constant payment value, the interest and principal payments are not equivalent in every period. Rather, because interest is in part determined by the principal value, a greater proportion of the payment shifts towards the principal payments as more of the principal is paid off over time.

- Principal Payments → The principal payments, otherwise known as the amortization of the loan, is the gradual reduction in the loan’s outstanding balance. In short, each principal payment reduces credit risk because the capital is returned to the original owner.

The repayment of principal is the return of borrowed capital, so the upside in yield comes from the interest rate (and to reiterate, the value of the interest payments is based on the outstanding principal). However, the capital at risk, i.e. the potential downside, is the loan principal.

Excel PMT vs. PPMT vs. IPMT Function

Two common Excel functions closely related to the “PPMT” function are “PMT” and “IPMT”.

- “=PMT” → The “PMT” function in Excel calculates the periodic payment on a loan, inclusive of both the interest and principal.

- “=IPMT” → In contrast, the “IPMT” in Excel calculates only the interest paid on a loan, as suggested by the “I” in front that stands for “interest.”

The missing piece between the above two functions is the principal payments, which the PPMT function is intended to calculate.

- IPMT Function → Interest

- PPMT Function → Principal

- PMT Function → Principal + Interest

However, it is important to note that there are often other fees and incurred costs such as taxes that can impact the lender’s yield.

Excel PPMT Function Formula

The formula for using the PPMT function in Excel is as follows.

=PPMT(rate, per, nper, pv, [fv], [type])

The brackets around “fv” and “type” denote that the two are optional inputs that can be omitted, i.e. left blank.

In terms of the sign convention, the interest and principal payments represent “outflows” of cash to the borrower, so the returned values will be expressed as negative numbers.

The following table can be referenced to confirm the interest rate and number of periods are adjusted properly for the units to be consistent.

| Payment Frequency | Interest Rate Adjustment | Number of Periods Adjustment |

|---|---|---|

| Monthly |

|

|

| Quarterly |

|

|

| Semi-Annual |

|

|

| Annual |

|

|

For example, imagine a borrower took out an 8-year loan with an annual interest rate of 6.0% paid on a quarterly basis. In this case, the adjusted (i.e. quarterly) interest rate is 1.5%.

- Monthly Interest Rate (rate) = 6.0% ÷ 4 = 1.5%

The number of periods must also be adjusted for the periodicity to match.

The borrowing term in our example was stated in years, so we must multiply it by the payment frequency, i.e. the number of compounding periods, or quarters.

- Number of Periods (nper) = 8 Years × 4 = 32 Periods

PPMT Excel Function Syntax

The table below describes the syntax of the Excel PPMT function in more depth.

| Argument | Description | Required? |

|---|---|---|

| “rate” |

|

|

| “per” |

|

|

| “nper” |

|

|

| “pv” |

|

|

| “fv” |

|

|

| “type” |

|

|

PPMT Function Calculator – Excel Model Template

We’ll now move on to a modeling exercise, which you can access by filling out the form below.

Step 1. Principal Payment on Loan Exercise Assumptions

Suppose a consumer has taken out a $10,000 personal loan with a stated annual interest rate of 6.00%, with monthly payments due at the end of each month.

- Loan Principal (pv) = $10,000

- Annual Interest Rate (%) = 6.00%

- Borrowing Term = 2 Years

- Compounding Frequency = Monthly (12x)

The next two steps are to convert our 6.0% annual interest rate into a monthly interest rate, followed by converting our 2-year borrowing term into months.

Using the following equations, we calculate the monthly interest rate as 0.50% and the number of periods as 24 months.

- Monthly Interest Rate (rate) = 6.00% ÷ 12 = 0.50%

- Number of Periods (nper) = 2 Years × 12 = 24 Periods

Step 2. Payment Frequency and “nper” Calculation

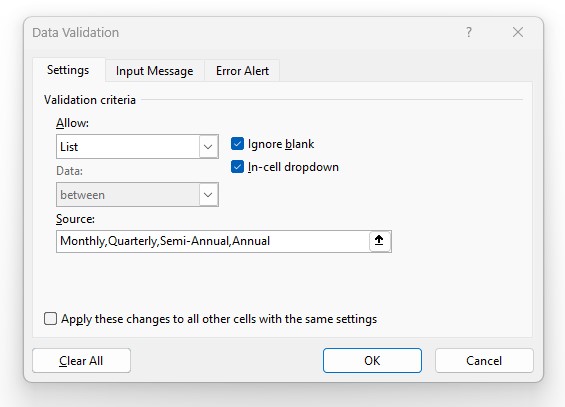

While optional, we’ll create a drop-down list to switch between the payment frequencies using the following steps:

- Step 1 → Select the “Compounding Frequency” Cell (E8)

- Step 2 → Click “Alt + A + V + V” to Open the Data Validation Settings Box

- Step 3 → Pick “List” in the Criteria Section

- Step 4 → Enter “Monthly”, “Quarterly”, “Semi-Annual”, or “Annual” into the “Source” line

In the cell below our drop-down list cell, we’ll enter a formula with a string of “IF” statements to return the figure that corresponds to our active selection.

=IF(E8=”Monthly”,12,IF(E8=”Quarterly”,4,IF(E8=”Semi-Annual”,2,IF(E8=”Annual”,1))))

In effect, if we set our active cell to “Monthly”, our annual interest rate (6.00%) will be divided by 4 while the number of periods (2 Years) is multiplied by 4.

- Monthly Interest Rate = 0.50%

- Number of Periods (nper) = 24 Periods

Step 3. “fv” and “type” Optional Arguments

The “fv” and “type” are the remaining two arguments, both of which we’ll omit here for the following reasons:

- ”fv” → Our assumption for the future value will be left blank as we anticipate the consumer to fulfill all obligations related to the debt and not default, so the value of the loan at maturity should be zero.

- “type” → The timing of the payments was stated earlier as being due at the end of each month, meaning that we can omit it since the default setting in Excel is already set to the end of the period.

Step 4. “per” and Principal Payment Calculation Example

Given the assumptions from the prior steps, we now have the necessary inputs to build our two-year principal payment schedule.

The PPMT formula in Excel for Period 1 is the following:

=PPMT($E$6,B13,$E$10,$E$4)

All the arguments, aside from the “per” input, are absolute cell references (F4). The interest rate (”rate”), number of periods (”nper”) and present value (”pv”) are all fixed values that should be kept constant.

Once Period 1 is complete, we can copy-paste the formula down our table (or drag it down) until we reach 24 periods.

Step 5. Principal Payment Schedule Table (=PPMT)

In the final step, we’ll calculate the sum of all principal payments from Period 1 to Period 24.

The total principal payment is ($10,000), confirming our calculation is correct, since the principal value of the loan at issuance was also $10,000.

Turbo-charge your time in Excel

Used at top investment banks, Wall Street Prep’s Excel Crash Course will turn you into an advanced Power User and set you apart from your peers.

Learn More